BRRRR in 2021, Is Not BRRRR in 2026

Read Time: 5-8 minutes

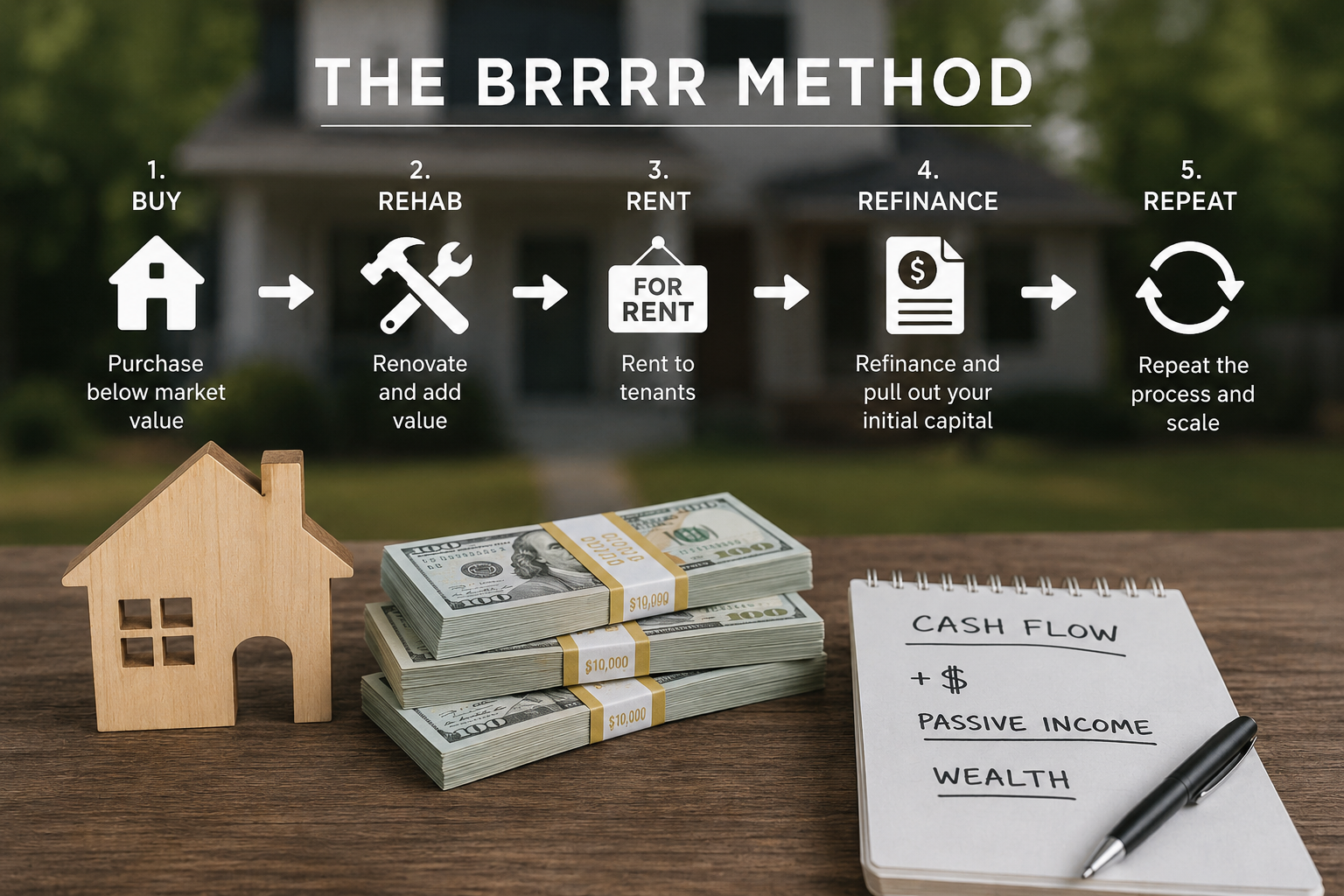

There was a moment, roughly 2019 through early 2022, when the BRRRR strategy felt almost foolproof. Buy a distressed property, rehab it, rent it out, refinance at a higher appraised value, and repeat. With 30-year fixed rates sitting below 3.5% and labor cheap and plentiful, the math worked on deals that, frankly, didn't deserve to work. Thin margins got papered over by cheap debt and rising values. Investors confused a favorable macro environment with personal skill. That environment is gone. And investors who haven't updated their mental model are getting hurt.

In 2026, BRRRR still works, but only if you underwrite like the conditions you're actually operating in, not the ones you remember.

What the Numbers Look Like Now

Let's start with the baseline that makes everything downstream harder.

In 2021, a savvy investor could refinance a stabilized rental into a 30-year fixed loan at 3.25%–3.75%. Today, conventional investment property rates are running 7.0%–7.75%, and DSCR loans, the go-to for BRRRR investors doing multiple deals, are pricing between 7.5% and 8.25% depending on LTV and reserves.

That spread isn't trivial. On a $200,000 refinance:

At 3.5%: ~$898/month principal and interest

At 7.75%: ~$1,432/month principal and interest

That's $534/month in additional debt service on a single property. If your pro forma assumed $1,400/month rent in a B-class Kansas City market, you had comfortable positive cash flow in 2021. In 2026, you're barely breaking even before vacancy, maintenance, and property management fees, and that's assuming the appraisal comes in where you need it.

Failure Mode #1: Appraisal Risk

The "R" that kills deals in 2026 is the refinance appraisal, and it's killing them in two ways.

First, values have softened in many investor-heavy markets. After years of appreciation driven partly by institutional buying, some Midwest markets that BRRRR investors flocked to such as Kansas City, Indianapolis, Memphis, have seen modest corrections or flat appreciation in 2025–2026. The "forced equity" thesis still holds if your rehab is excellent, but you can no longer count on market appreciation to backstop a mediocre renovation.

Second, lender conservatism has increased. DSCR lenders are stress-testing appraisals harder than they were two years ago. Appraisal management companies are under pressure to be conservative after the regulatory scrutiny of 2023–2024. Deals that would have sailed through at a $250,000 ARV are coming back at $225,000, which means the refinance doesn't pull out your full renovation investment, which means you're leaving capital in the deal, which means your actual cash-on-cash return and the speed of your "repeat" cycle both suffer.

The fix: Stop underwriting an optimistic ARV. Find three legitimate comps, average them, then run your numbers at 90% of that figure. If the deal still works, you have margin. If it doesn't, you're not passing on a good deal. You're passing on a risky one that looks good on paper.

Failure Mode #2: Rehab Timeline Blowout, and What It Costs You Beyond Money

Rehab timelines have always carried risk. In 2026, there's a specific, underappreciated driver of delays that most investors outside the construction industry aren't tracking closely enough: immigration-related labor shortages.

Since late 2024, enforcement actions and policy changes at the federal level have meaningfully thinned the construction labor pool in many markets. Subcontractors who relied heavily on immigrant labor, particularly in roofing, drywall, framing, and finish work, are stretched thin or simply unavailable at the price points investors budgeted. The crews that exist are booked out further, their prices have risen, and when a job runs into a snag, they're slower to return because they have other work waiting.

What does this mean practically? A rehab you budgeted for 60 days is running 90–120 days in many Kansas City-area markets as of early 2026. That's not a contractor problem. That's a market condition.

The financial cost is obvious: carrying costs stack up. Financing a purchase and renovation at 10–12% hard money for four extra months on a $150,000 project is $5,000–$7,500 you didn't budget. Worse, if you're using a bridge lender with extension fees, it gets uglier fast.

But here's the failure mode investors are sleeping on: bonus depreciation and placed-in-service deadlines.

Under current tax law (as extended and modified through the Inflation Reduction Act adjustments), investors pursuing cost segregation and bonus depreciation need their property placed in service. That means rent-ready and available for rent by December 31 of the tax year in which they want to claim the deduction. A rehab that bleeds from September into January doesn't just cost you carrying costs. It can push your entire cost segregation benefit into the following tax year, disrupting your tax planning and, in some cases, costing you the ability to offset other income at the rate you planned.

If bonus depreciation is part of your deal's financial thesis, then rehab timeline risk is a tax risk, not just construction risk. Model it that way.

The fix: Build in a 30–40% timeline buffer on all rehab estimates. Establish relationships with two or three reliable crews before you need them, not after. And if you're counting on placed-in-service status for a specific tax year, don't close on a property requiring significant rehab after October 1 unless you have iron-clad contractor commitments and a clear-eyed backup plan.

Failure Mode #3: The Over-Leveraged Refinance

This one is structural, and it's a direct consequence of the rate environment.

In 2021, pulling 75–80% LTV out of a refinanced BRRRR property left you with positive cash flow and a cushion. At 3.5%, the debt was cheap enough that high leverage was manageable. Investors got conditioned to the idea that maximum cash-out was always the right move.

At 7.5–8%, maximum cash-out is often a trap.

Here's a realistic 2026 scenario. You buy a Kansas City duplex for $85,000, put $45,000 into a solid rehab, and end up with an all-in basis of $135,000 (including closing costs and carrying costs). The property appraises at $175,000. A 75% LTV refinance pulls out $131,250, close to a full capital recycle, and on paper that looks like a win.

But now model the cash flow:

Gross rent: $2,200/month (two units at market rate)

Property management (9%): -$198

Vacancy allowance (8%): -$176

Maintenance reserve: -$150

Insurance + taxes: -$350

Debt service ($131,250 at 7.75%, 30yr): -$939

Net monthly cash flow: +$387

That's a 3.4% cash-on-cash return on the roughly $4,000 in equity you left in the deal. The headline numbers look fine, but you've created a property that will go cash-flow negative at the first major repair; a roof, an HVAC replacement, a vacancy of more than a month. You've also left yourself with essentially no equity cushion if values soften further.

The investors who are building durable portfolios in 2026 are refinancing to 65–70% LTV, accepting that they'll leave more capital in the deal, and targeting cash flows in the $500–$700/month range per property before they feel comfortable moving on. The "repeat" cycle is slower. That's the right trade-off right now.

What Still Works: The Discipline Premium

None of this means BRRRR is dead. It means the spread between disciplined and undisciplined investors has widened dramatically.

The investors winning in Kansas City, and in comparable Midwest markets in 2026 share a few traits:

They have a local team they trust, not just contractors they found online. A property manager who gives you honest rent comps before you buy, a local lender who knows DSCR products cold, an inspector who actually knows the housing stock in your target zip codes, this is not optional infrastructure anymore. It's the difference between hitting your numbers and missing them.

They're buying deeper. In 2021, a deal at 70 cents on the dollar worked. In 2026, you need to be at 55–65 cents to have the margin to absorb appraisal variance, timeline blowout, and higher debt service. That means being more selective, making more offers, and walking away from deals that would have "worked" two years ago.

They're underwriting conservatively on every variable simultaneously. Not just ARV or just rent, every variable. Conservative ARV, conservative rent (use current actuals, not peak comps from 2023), full timeline buffer, full expense load. If the deal clears all of those hurdles, it's a real deal.

They're thinking about tax strategy before they close, not after. Cost segregation, placed-in-service timing, and depreciation recapture on the eventual sale all need to be part of the underwriting conversation with your CPA, not an afterthought.

The Bottom Line

BRRRR built a lot of wealth between 2015 and 2022 partly because the strategy is sound and partly because the macro environment was extraordinarily forgiving. The investors who mistake that era's results for a template are the ones posting in forums about "my contractor ghosted me" and "the appraisal came in low" and "the cash flow isn't there." The investors building real portfolios in 2026 have recalibrated. They're doing fewer deals, making more money per deal, and sleeping better at night.

The strategy didn't break. The conditions changed. Adjust accordingly.

Data and market observations drawn from Alpine Property Management Kansas City, February 2026. Investment performance varies by market, asset class, and operator. This post is for informational purposes only and does not constitute investment or tax advice. Consult a licensed CPA and financial advisor before making investment decisions.

Source: February 2026 data, Alpine Property Management Kansas City